By Dr. James M. Minnich

Honolulu, Hawaii — March 24, 2026

Modern power depends on materials most people never see. Critical minerals and rare earth elements (REEs) underpin advanced defense manufacturing, semiconductors, batteries, precision guidance systems, and secure communications infrastructure. They are invisible sinews of economic strength and military capability.

Yet their importance is often misunderstood. The strategic question is not simply who possesses these resources. It is who controls the system through which they are processed, priced, and delivered. In a world of “just-in-time” efficiency, that distinction has become a matter of strategic consequences.

In a recent discussion during Episode 4 of Strategic Voices at the Daniel K. Inouye Asia-Pacific Center for Security Studies, Professor Andrea Malji and I examined what this evolving environment means for regional strategy. Our conclusion was clear: The era of passive markets is over.

From Abundance to Vulnerability

The United States identified 35 critical mineral commodities in 2018 under Executive Order 13817. By November 2025, that list had nearly doubled to 60, covering more than half of the periodic table. This expansion reflects a sobering reality: modern economies rely on a far broader set of materials than previously understood.

Within this group, rare earth elements occupy a central position. These 17 elements enable high-performance permanent magnets, advanced electronics, and energy systems. In 2023, permanent magnets alone accounted for over 45 percent of global rare earth demand, powering everything from smartphones and MRI machines to electric vehicles and jet aircraft.

These materials are not “rare” in a geological sense; they are widely distributed across the globe. What is rare is the industrial capacity—and the environmental tolerance—to process them at scale.

The Geography of Control

Today, the Indo-Pacific sits at the center of this system. While mineral deposits are geologically dispersed—found from Australia and the United States to Vietnam, Brazil, and Africa—the capacity to turn “dirt” into “technology” is industrially concentrated.

China currently dominates the processing of 85 percent of the world’s rare earth elements and refines roughly 60% of global lithium. This concentration creates a structural bottleneck. The shipping routes that carry these materials—the South China Sea, the Taiwan Strait, and the Straits of Malacca—form a narrow set of critical corridors through which global trade flows. This is not a supply problem; it is a system-design problem where the processor holds a veto over the producer. In the Indo-Pacific, where production, processing, and transit converge, these dynamics are not abstract—they are operational.

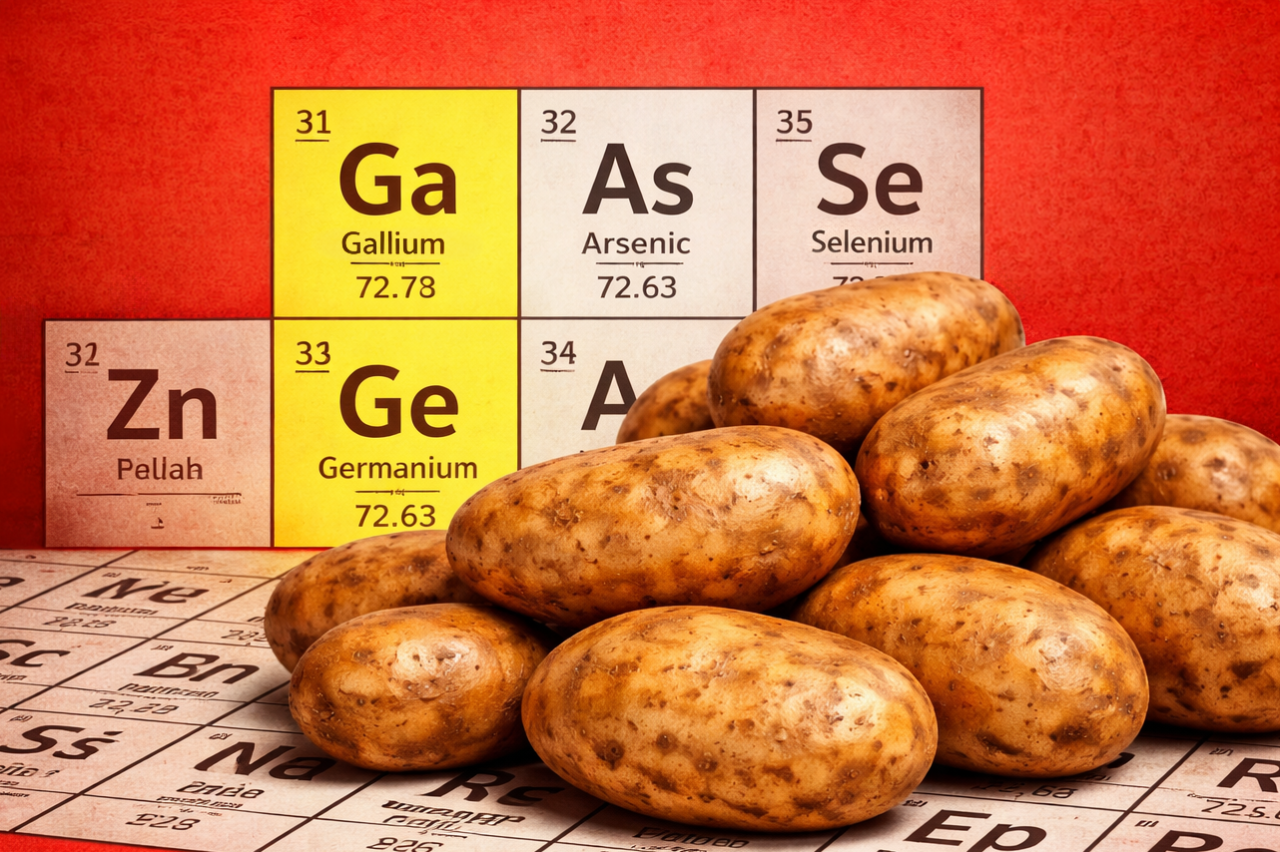

The “Potato Logic” of Power

Professor Shyam Tekwani described this dynamic as the “potato logic of power.” The lesson is historical and haunting. In nineteenth-century Europe, reliance on a single, high-yield crop—the Lumper potato—created a system that was efficient, scalable, and invisible.

When the blight arrived in 1845, it did not create the vulnerability; it revealed it. The system had no redundancy. Today’s critical mineral supply chain is the digital age’s Lumper potato. Supply chains optimized solely for cost and efficiency have concentrated capacity in a handful of locations. For decades, this appeared stable. Materials flowed. Markets functioned. Alternatives were deemed “inefficient.”

Then, in 2023, the blight arrived in the form of export controls. China introduced restrictions on gallium and germanium—materials essential to radar and satellite technologies. China accounts for 98 percent of global gallium production. The announcement was brief, but the leverage was absolute. Prices adjusted instantly, not because of scarcity in the earth, but because of control over the gate.

The Extraction Trap

The Democratic Republic of the Congo (DRC) remains the epicenter of cobalt production, yet the ownership structure reveals a stark geopolitical reality: 15 of its largest 19 mines are under Chinese control or financing. While the DRC provides raw ore, the true center of gravity remains the midstream refining stage. It is here that the material is transformed into battery-grade chemicals, granting the processors—rather than the miners—ultimate control over the high-tech supply chain.

As Professor Andrea Malji explained, Indonesia attempted to change this equation by banning nickel ore exports and requiring domestic refining. While the policy shifted industrial activity onshore, much of the new refining capacity is operated by foreign firms. The geography has shifted, but the logic of control remains contested. Resource ownership does not guarantee strategic autonomy; more often, it introduces new, complex dependencies.

The U.S. Response: Designing a New System

Washington is now attempting to move beyond mere supply toward system design. Through initiatives like Project Vault, price-floor mechanisms, and the Forum on Resource Geostrategic Engagement (FORGE), the U.S. and its partners are using industrial policy to stabilize markets and incentivize alternative processing networks.

This is a significant pivot. Rather than relying on “blind” markets, the United States is shaping outcomes—a return to the strategic mobilization seen during the mid-twentieth century. However, as Gracelin Baskaran notes, “history” offers a caution. Throughout the 1900s, the United States mobilized in crisis only to dismantle its capacity once stability returned. Stockpiles were sold; expertise eroded. The challenge today is not just launching these initiatives—it is the political will to sustain them.

The Quiet Nature of Leverage

In this new environment, power is rarely exercised through total disruption. It appears as administrative friction: slower export approvals, licensing delays, and technical requirements. These mechanisms do not halt supply chains; they shape them. They signal the conditions under which access will be granted.

Critical minerals have become instruments of statecraft functioning below the threshold of conflict. They allow states to influence geopolitical outcomes without firing a shot.

Conclusion: Who Sets the Price?

The central question remains: Who defines the terms under which those resources are accessed and exchanged?

In this context, price is not just a market signal; it is an expression of power. It reflects control over processing capacity and authority over market rules. The contest over critical minerals is not a “gold rush” for deposits. It is a competition to build the architecture of the 21st-century economy. In this competition, the decisive advantage lies not with those who extract the resource—but with those who control the system that gives it value.

Referenced in this Episode:

- Andrea Malji, Critical Minerals and Coercive Power in the Indo-Pacific.

- Shyam Tekwani, The Potato Logic of Power.

- Nicolas Niarchos, The Elements of Power.

This article reflects the author’s analysis and does not represent the views of any institution or individual.

{kind=link}

{kind=link}

{kind=link}

Leave A Comment